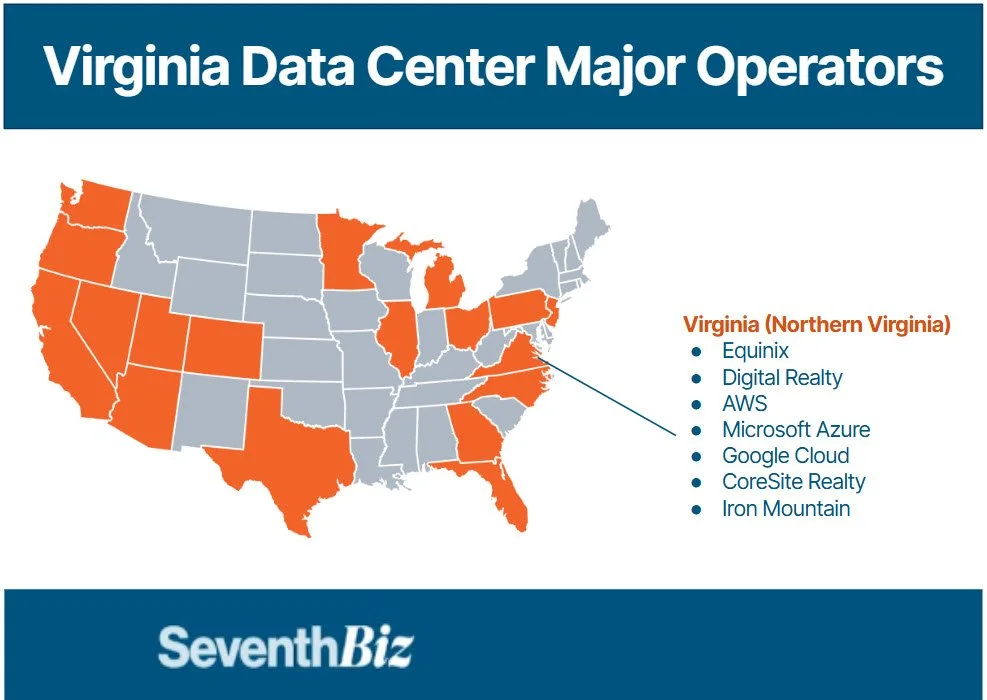

A 30-year head start. Northern Virginia’s rise began in the 1990s when early internet exchange points clustered around D.C. and spilled into Loudoun and Fairfax counties. That interconnection density attracted carriers, then colocation operators (notably the first large Equinix campus in Ashburn), and later hyperscalers. State and county policy reinforced the flywheel: a long-standing sales-and-use tax exemption on qualifying data center equipment, comparatively efficient permitting in business-friendly counties, and a deep bench of fiber, construction, and facilities talent created compounding network effects.

Power, proximity, and policy. Two ingredients then scaled the advantage. First, low-latency proximity to the federal government and East-Coast population centers made Northern Virginia a default first stop for enterprise and cloud footprints. Second, utility planning and transmission capacity—while now stressed—enabled multi-gigawatt campuses to phase in over time. Each new cluster reduced interconnection costs for the next, locking in the region’s leadership as “Data Center Alley.”

The Market Today: Scale, Stress, and a Sprawl Effect

Scale that sets global benchmarks. Northern Virginia is still the largest data center market in the world by megawatts delivered and in-flight. Absorption remains dominated by a handful of hyperscale buyers, while wholesale colocation continues to pre-lease far ahead of delivery. Land values around established nodes (Ashburn, Sterling, Manassas) have re-rated meaningfully, and viable greenfield tracts near high-capacity substations are scarce.

Power is the new zoning. The binding constraint is interconnection and transmission, not tenant demand. Utilities are creating bespoke rate classes and planning multi-year grid upgrades to serve AI-driven loads. Developers with firm power positions, adjacent substation optionality, or credible on-/near-site generation and storage have a durable edge. Capacity auction outcomes and fuel adjustments are feeding through to forward operating cost curves, making power procurement strategy as important as shell and fit-out.

The sprawl beyond Loudoun. Permitting risk and transmission bottlenecks are pushing growth south and east along existing rights-of-way and toward metros like Prince William, Henrico (Richmond area), and further into Southern Virginia locales with available land, favorable local tax treatment, and co-op utility partnerships. Where entitlements are contested, timelines and carrying costs are rising; where local policy is coordinated with utilities, time-to-power remains the key differentiator.

Virginia’s Governor’s Race: What the Outcome Could Mean for Data Center

Baseline to assume: Virginia’s long-running posture has balanced growth with guardrails. The election outcome does not change underlying demand from cloud and AI workloads; what it can influence are cost of power, permitting velocity, and incentive shape. Three practical scenarios to watch:

“Conditioned incentives” over “open-ended incentives.” Expect continuity on the equipment sales-and-use exemption framework, with a higher likelihood of eligibility tightening (energy-efficiency thresholds, reporting, or community-benefit conditions). For developers, this mostly affects underwriting (qualification risk, compliance costs) rather than headline feasibility.

Faster grid investment paired with stronger cost-allocation pushes. AI load growth already requires large transmission and generation spend. A Democratic administration is more likely to lean into build-out (transmission, storage, and clean power) while pressing for data centers to “pay their share,” via targeted rate classes, rider structures, or proffers when local impacts are material. Net effect: higher all-in power costs for greenfield campuses lacking locked contracts, partly offset by improved delivery certainty and reputation benefits from cleaner supply.

Land-use and siting: more predictability where plans are aligned, longer timelines where they aren’t. Highly contested mega-corridors will face tighter procedural scrutiny; counties with updated comp plans, industrial overlays, and utility-backed capacity maps will move faster. For investors, this favors portfolio strategies with multiple sites across counties/utilities and option-style control on parcels adjacent to robust transmission.

Bottom line for capital allocation. The demand signal (cloud + AI) is durable; Virginia’s comparative advantages remain formidable. Policy drift points to modestly higher capex/opex and more structured incentives, but also to clearer rules of the road for power-constrained projects. Sponsors that secure long-lead power, embed efficiency and onsite-resource plans, and cultivate county-utility alignment should continue to out-compete on delivery and returns.

Data center demand in Virginia is part of a much larger national acceleration. Hyperscale and AI workloads are driving record leasing, record pre-commitments, and a shift from “build it and lease it” to “lease it before it’s built.” For investors, developers, and operators trying to understand where capital is flowing next, our flagship industry analysis—Data Centers in the AI Era: Navigating Growth, Energy Challenges, and Digital Transformation—breaks down the economics behind this surge. The report covers market size, growth drivers, power constraints, REIT dynamics, tax incentives, and the evolution of hyperscale and AI-optimized facilities. It also maps where demand is shifting as power availability becomes the new limiting factor.

If you’re evaluating sites, investment theses, or partnerships in digital infrastructure, this report provides:

A full industry primer (market size, TAM, and regional growth hubs)

Financial and operational dynamics (power costs, CapEx/OpEx structure, REIT advantages)

Competitive landscape across hyperscale, colo, edge, and AI-accelerated facilities

Analysis of grid strain, energy procurement, and sustainability requirements

A directory of operators, vendors, investors, utilities, and ecosystem partners

You can access the report here:

👉 Data Centers in the AI Era: Navigating Growth, Energy Challenges, and Digital Transformation

We’ll be releasing a Virginia-focused deep dive next—mapping substations, power constraints, and development windows across Northern Virginia and emerging submarkets.